Thinking about buying a home or refinancing your mortgage? Understanding how your interest rate affects your monthly payments can save you money and stress.

A variable interest rate mortgage might be the key to unlocking more flexible and potentially lower payments, but it also comes with some risks you need to know. You’ll discover exactly what a variable interest rate mortgage is, how it works, and whether it’s the right choice for your financial future.

Keep reading to make smarter decisions about your mortgage and take control of your home loan journey.

Variable Interest Rate Basics

A variable interest rate mortgage means your interest rate can change over time. This type of mortgage is also called an adjustable-rate mortgage (ARM). The rate usually starts low but can go up or down based on market conditions.

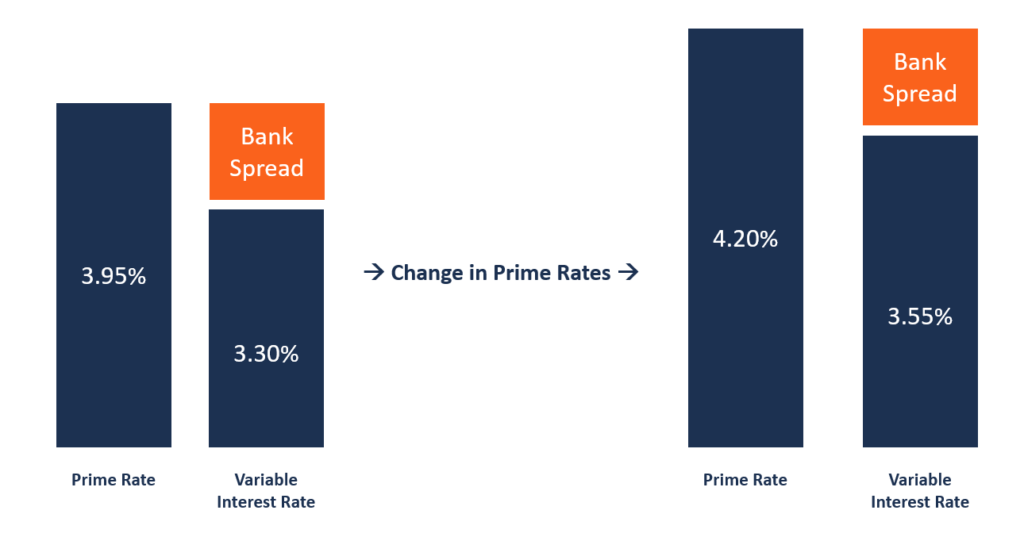

Rates are often tied to an index like the prime rate or LIBOR. Lenders add a set amount called a margin to this index to decide your total rate. Changes in the index cause your mortgage rate to change.

| Fixed Rate Mortgage | Variable Rate Mortgage |

|---|---|

| Interest rate stays the same for the loan term | Interest rate changes based on market indexes |

| Monthly payments stay constant | Monthly payments can rise or fall |

| Good for budgeting and stability | Potential for lower initial payments |

| Usually higher starting rate | Usually lower starting rate |

Advantages Of Variable Rate Mortgages

Variable rate mortgages often start with lower initial rates than fixed loans. This can mean smaller monthly payments at the beginning. If interest rates drop, your payments may go down, saving you money over time.

This type of mortgage offers flexibility. It adapts to the changing market conditions, which can be good if rates decrease. You can benefit from lower costs without needing to refinance.

Still, rates can rise, which means payments might increase too. But the chance to save when rates fall is a key advantage for many borrowers.

Risks To Consider

Rate increases can raise your monthly mortgage payments. This makes budgeting difficult and causes stress. Payment changes may happen unexpectedly, affecting your monthly expenses.

Economic shifts impact interest rates. When the economy improves, rates often rise. During downturns, rates might fall. These changes affect how much you pay each month.

Planning finances for the long term can be tricky. Uncertain rates mean future payments are unknown. It is hard to predict total mortgage costs over many years.

How To Choose The Right Mortgage

Start by looking at your income and monthly expenses. Know how much you can pay each month without stress. Consider any future changes in your finances, like a new job or family plans.

Check recent interest rate trends. Variable rates can rise or fall, so study the market carefully. Think about how rate changes may affect your payments over time.

| Loan Feature | What to Compare |

|---|---|

| Interest Rate | Initial rate, how often it changes, max rate |

| Loan Term | Length of loan and payment schedule |

| Fees | Closing costs, penalties, and extra charges |

| Flexibility | Options for early repayment or refinancing |

Tips For Managing A Variable Rate Mortgage

Keep track of interest rate changes by checking your lender’s updates regularly. Small changes can affect your monthly payments. Staying informed helps plan your budget better.

Plan for payment ups and downs. Set aside extra money each month to cover higher payments. This buffer reduces stress during rate increases and keeps your finances stable.

Explore refinancing options if rates rise too much. Refinancing can lock in a lower rate or switch to a fixed rate. Compare offers from different lenders for the best deal.

:max_bytes(150000):strip_icc()/arm.asp-Final-45bee660c4a343e0a83eabdbb86a2e74.png)

Variable Rate Mortgages In Austin, Texas

Austin’s housing market is dynamic, with interest rates that often change. Variable rate mortgages in Austin follow the national trend but can vary due to local factors like economy and demand. Rates might rise or fall based on economic shifts, impacting monthly payments. This flexibility can suit buyers who expect rates to drop or plan to sell before rates rise.

| Popular Lenders | Current Offers |

|---|---|

| Wells Fargo | Low initial rates with periodic adjustments |

| Chase | Competitive variable rates with flexible terms |

| Bank of America | Discounts for good credit scores and loyalty |

Austin residents benefit from strong consumer protections under Texas law. Regulations require lenders to clearly explain how rates change and how much payments could increase. Borrowers receive notices before rate adjustments. These rules help buyers avoid surprises and understand their mortgage terms well.

Frequently Asked Questions

What Is The Current Mortgage Variable Rate?

The current mortgage variable rate varies by lender and market conditions. Check with your bank or financial institution for the latest rate. Variable rates fluctuate based on economic factors and benchmark indexes. Always compare offers to find the best variable mortgage rate available today.

Is It A Good Idea To Get A Variable Rate Mortgage?

A variable rate mortgage can save money if interest rates drop. It carries risk since rates may rise, increasing payments. Consider your financial stability and market trends before choosing.

What’s The Variable Interest Rate Right Now?

The current variable interest rate varies by lender and market conditions. Typically, it ranges between 5% and 7% annually. Check with your specific lender for the most accurate, up-to-date rate. Variable rates adjust periodically based on benchmark indexes like the prime rate or LIBOR.

Will Interest Rates Drop To 3% Again?

Interest rates may not drop to 3% soon due to current economic conditions and inflation trends. Rates depend on market factors and Federal Reserve policies. Watch for changes in economic data and central bank decisions that influence mortgage rates.

Conclusion

A variable interest rate mortgage lets your interest change over time. Rates may rise or fall with the market. This can lower your payments or increase them. It suits those who can handle some risk. Understanding how it works helps you decide.

Compare it with fixed-rate loans carefully. Choose the option that fits your budget. Stay informed about market trends for best results.

Read More

- Refinance Rate Lock Options: Secure Your Best Mortgage Deal Today

- Fixed Rate Mortgage Offers: Unlock Best Deals for Homebuyers Today

- Low Apr Loan Comparison: Find the Best Deals Today

- Money Market Account Comparison: Top Rates and Benefits Revealed

- Private Banking Interest Offers: Unlock Exclusive High-Yield Benefits

- Home Equity Refinance Quotes: Unlock Savings with Top Rates Today

- Same Day Loan Prequalification: Fast, Easy Approval Tips

- Online Installment Loan Quotes: Unlock Fast, Easy Financing Today

- Prime Lending Rate Forecast: What Experts Predict for 2026

- Mortgage Refinance Approval Guide: Insider Tips for Fast Success