Thinking about tapping into your home’s value? Getting the right home equity refinance quotes can save you hundreds or even thousands of dollars.

But how do you find the best deal without wasting time or getting overwhelmed? This article will guide you step-by-step to compare offers easily and confidently. By the end, you’ll know exactly what to look for and how to choose a quote that fits your financial goals perfectly.

Keep reading to unlock the full potential of your home’s equity with smart refinancing.

What Is Home Equity Refinance

Home equity refinance means replacing your current mortgage with a new one. This new loan uses the value built in your home as security. It lets you borrow money by tapping into your home’s equity. Many people use it to get a better interest rate or change loan terms.

Refinancing can help reduce monthly payments or allow you to borrow cash. The new loan pays off the old mortgage completely. The amount you can borrow depends on your home’s current market value and what you still owe.

Different types of home equity refinancing exist, like cash-out refinance or rate-and-term refinance. Each has different goals and benefits. Choosing the right one depends on your financial needs and home value.

How Refinance Saves You Money

Lower interest rates help reduce the total amount paid on your loan. This means you save money over time. Lenders often offer better rates for refinancing because your home’s value helps secure the loan.

With reduced monthly payments, you get more budget flexibility. Smaller payments make it easier to cover other expenses or save for future needs. Refinancing can stretch your payments over a longer time, lowering each month’s cost.

Tax benefits come from the interest you pay on your home equity loan. This interest might be deductible on your federal tax return. Always check current tax rules or ask a tax professional for advice.

Types Of Home Equity Refinance

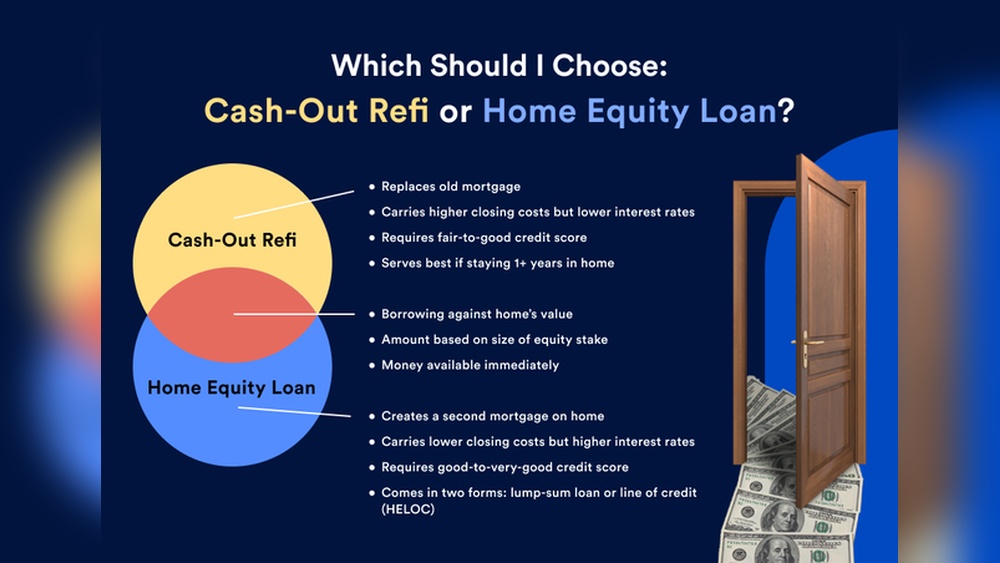

Cash-Out Refinance lets homeowners borrow extra money by refinancing for more than the current loan balance. The difference is given in cash for expenses like home repairs or debt payoff. It replaces the existing mortgage with a new one at a possibly lower rate.

Rate-and-Term Refinance focuses on changing the loan’s interest rate or term without taking extra cash. It helps reduce monthly payments or shorten the loan duration. This option is good for saving on interest over time.

Home Equity Line of Credit (HELOC) is a revolving credit line based on home equity. Borrowers can take money as needed, paying interest only on the amount used. It offers flexibility for ongoing or unexpected costs.

:max_bytes(150000):strip_icc()/homeequityloan-e11896bf4ac1475a9806a55f92e0c312.jpg)

Factors Affecting Refinance Rates

Credit score plays a big role in refinance rates. A higher score means better rates. Lenders see good credit as less risky. Scores below 620 may lead to higher rates or denial.

The loan-to-value (LTV) ratio shows how much you owe versus your home’s worth. Lower LTV means lower rates. If you owe less than 80% of your home’s value, you may get better offers.

Market interest trends affect all refinance rates. When rates rise, refinancing costs more. When rates drop, refinancing becomes cheaper. Watching these trends helps find the best time to refinance.

Where To Find Top Refinance Quotes

Banks and credit unions offer reliable refinance quotes. They often provide stable rates and personal service. Credit unions usually have lower fees but require membership.

Online lending platforms make it easy to compare multiple offers. These platforms offer fast quotes and flexible options. Some may have higher rates, so read terms carefully.

Mortgage brokers work with many lenders to find the best deals. They save time by shopping around for you. Brokers may charge fees, but can help with complex cases.

Comparing Refinance Offers

Interest rates show the cost of borrowing money. They usually appear as a simple percentage. APR (Annual Percentage Rate) includes interest plus fees. APR gives a better idea of total loan cost. Lower interest rates may have higher APR if fees are big.

Closing costs and fees can add up. These include appraisal fees, title insurance, and lender fees. Ask for a detailed list to avoid surprises. Some lenders offer low fees but higher interest rates.

| Loan Terms | Details |

|---|---|

| Loan Length | Shorter terms mean higher payments but less interest paid overall. |

| Prepayment Penalties | Check if you pay extra for early payoff. |

| Payment Options | Some loans allow flexible payments or interest-only periods. |

Common Refinance Mistakes To Avoid

Hidden fees can increase your refinance cost a lot. These fees include closing costs, appraisal fees, and origination charges. Always ask for a full list of fees before signing any papers.

Overborrowing may seem like extra cash now, but it can cause problems. Borrow only what you really need to avoid higher monthly payments and longer debt periods.

Checking your credit report is important. Errors in your credit history can lead to higher interest rates or even loan denial. Take time to fix any mistakes before applying.

Steps To Secure The Best Refinance Rate

Improving your credit profile can help you get a better refinance rate. Pay off debts and keep credit card balances low. Check your credit report for errors and fix them quickly. Lenders like to see steady income and a good payment history.

Gather all necessary documents before applying. These usually include your recent pay stubs, tax returns, bank statements, and current mortgage details. Having everything ready speeds up the process and shows lenders you are organized.

Request multiple refinance quotes from different lenders. Compare their interest rates, fees, and loan terms. This helps you find the best deal. Don’t hesitate to ask questions if something is unclear. A little research saves money.

When To Refinance Your Home Equity

Market timing affects home equity refinance success. Interest rates change often. Lower rates mean better deals. Watch the market to save money.

Personal financial goals guide refinance decisions. Need cash for repairs? Or want to lower monthly payments? Define your goals before acting. Refinancing fits best with clear plans.

Life events may change your needs. Marriage, new job, or college costs? These events can affect how much you borrow. Refinancing can help manage new expenses or debts.

Heloc Vs Home Equity Loan Vs Refinance

HELOCs offer flexible borrowing with a credit line. You can borrow and repay multiple times. This suits ongoing expenses. Home equity loans provide a lump sum with fixed payments. Good for one-time costs like renovations. Refinance replaces your mortgage with a new loan. Often lowers interest rates or changes loan terms.

| Option | Flexibility and Access | Cost | Best Uses |

|---|---|---|---|

| HELOC | Flexible credit line, borrow as needed | Variable rates, interest may rise | Ongoing projects, emergencies |

| Home Equity Loan | One-time lump sum | Fixed rates, predictable payments | Large one-time expenses |

| Refinance | Replaces mortgage, new loan terms | May have closing costs | Lower interest or monthly payments |

Frequently Asked Questions

How Much Would A $100,000 Home Equity Loan Cost Per Month?

A $100,000 home equity loan costs about $450 to $600 monthly. Exact payment depends on interest rate and loan term.

What Is The 2% Rule For Refinancing?

The 2% rule for refinancing means your new interest rate should be at least 2% lower than your current rate. This helps ensure savings outweigh refinancing costs.

What Is The Monthly Payment On A $50,000 Heloc?

The monthly payment on a $50,000 HELOC depends on the interest rate and repayment terms. For example, at 6% interest over 10 years, payments approximate $555. Payments vary with rates and borrowing periods, so check current offers for exact amounts.

Is A Heloc A Trap?

A HELOC is not a trap but requires careful management. Rising rates or overspending can cause financial strain. Use it wisely.

Conclusion

Getting home equity refinance quotes helps you find the best deal fast. Compare rates from different lenders before deciding. Lower interest rates can save you money over time. Choose a loan that fits your budget and goals. Take your time and ask questions if unsure.

Smart choices today lead to financial peace tomorrow.

Read More

- Refinance Rate Lock Options: Secure Your Best Mortgage Deal Today

- Fixed Rate Mortgage Offers: Unlock Best Deals for Homebuyers Today

- Low Apr Loan Comparison: Find the Best Deals Today

- Money Market Account Comparison: Top Rates and Benefits Revealed

- Private Banking Interest Offers: Unlock Exclusive High-Yield Benefits

- Same Day Loan Prequalification: Fast, Easy Approval Tips

- Online Installment Loan Quotes: Unlock Fast, Easy Financing Today

- Prime Lending Rate Forecast: What Experts Predict for 2026

- Mortgage Refinance Approval Guide: Insider Tips for Fast Success

- Low Interest Personal Loans: Unlock Affordable Borrowing Today