Looking to make your money work harder without locking it away? A money market account could be just what you need.

But with so many options out there, how do you choose the best one for your goals? In this comparison, you’ll discover how money market accounts stack up against savings accounts and other cash storage options. You’ll learn what to watch out for—like fees, interest rates, and access to your funds—so you can pick the account that suits your lifestyle and helps your savings grow faster.

Keep reading to find out how to get the most from your money market account and make every dollar count.

Top Money Market Rates

Current high-yield money market accounts often offer interest rates above 4%. Online banks usually provide higher APYs because they have lower costs. Traditional banks might offer better customer service and easier branch access.

Jumbo accounts require a larger minimum deposit, often $100,000 or more. They tend to have higher interest rates than regular accounts. This makes them good for people with large cash reserves.

| Type | Interest Rate | Minimum Deposit | Notes |

|---|---|---|---|

| Online Banks | 4.2% APY | $1,000 | Higher rates, no physical branches |

| Traditional Banks | 3.5% APY | $2,500 | Lower rates, branch access |

| Jumbo Accounts | 4.5% APY | $100,000 | Best for large deposits |

Key Features To Compare

Interest rates and APYs show how much money you can earn. Higher rates mean better returns. Look for accounts offering competitive APYs to grow your savings faster.

Minimum balance requirements tell you the least amount of money needed to open or keep the account. Some accounts need only a small amount, while others require a larger balance. Falling below this can lead to fees.

Monthly fees and charges can reduce your earnings. Many accounts have no fees if you maintain the minimum balance. Check if fees apply and how to avoid them.

Transaction and withdrawal limits affect how often you can move money. Most accounts limit transfers or withdrawals to six per month. Exceeding limits may cause extra charges or account changes.

Benefits Of Money Market Accounts

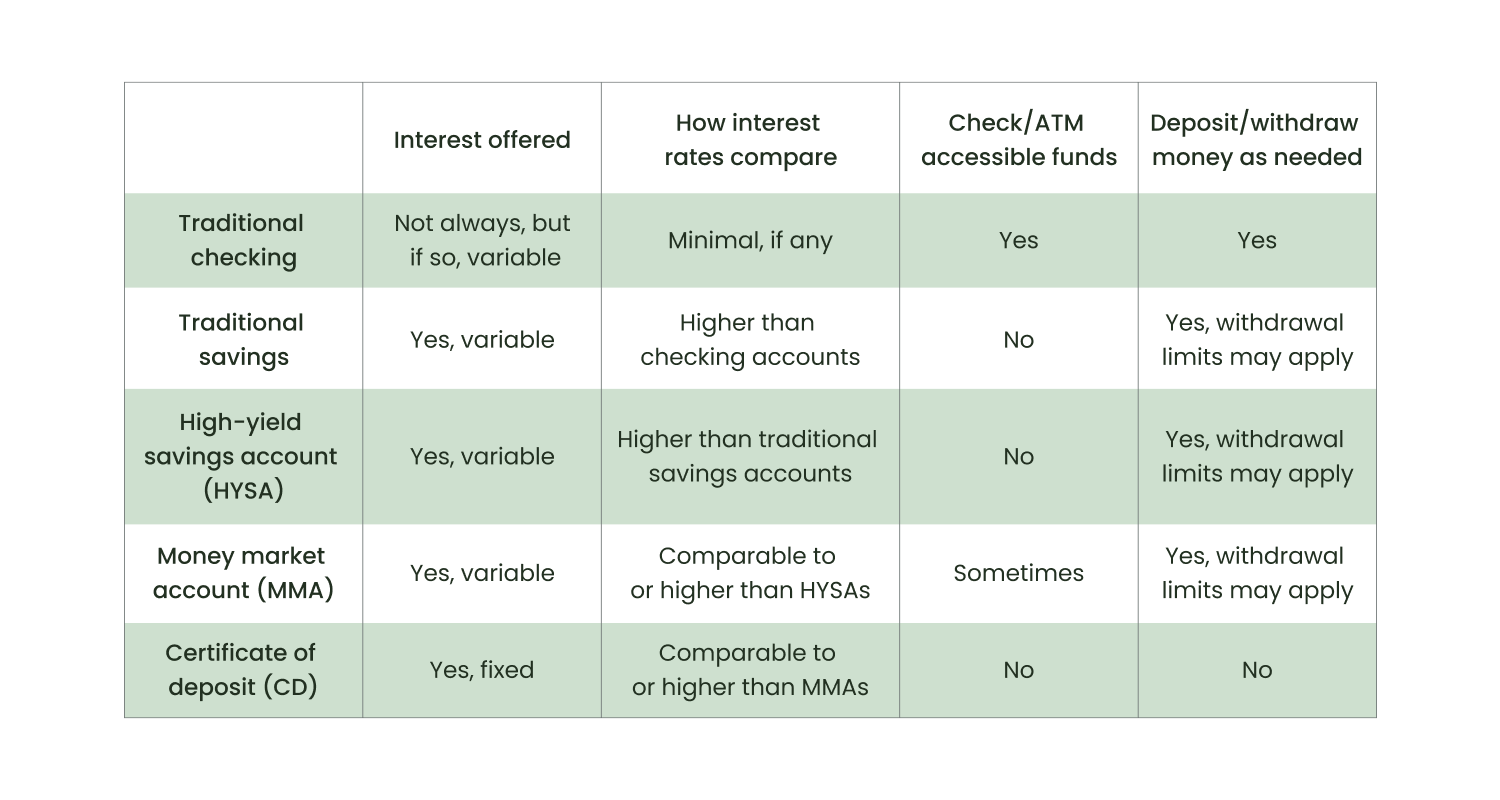

Money market accounts usually offer higher returns than regular savings accounts. This makes your money grow faster with less risk. They often allow check-writing and debit card access, giving you easy access to funds. Unlike some savings accounts, you can use checks or a debit card for payments.

FDIC insurance protection secures your deposits up to $250,000. This means your money is safe even if the bank faces trouble. You can withdraw money when needed, offering liquidity and flexibility. This makes money market accounts a good choice for both saving and spending.

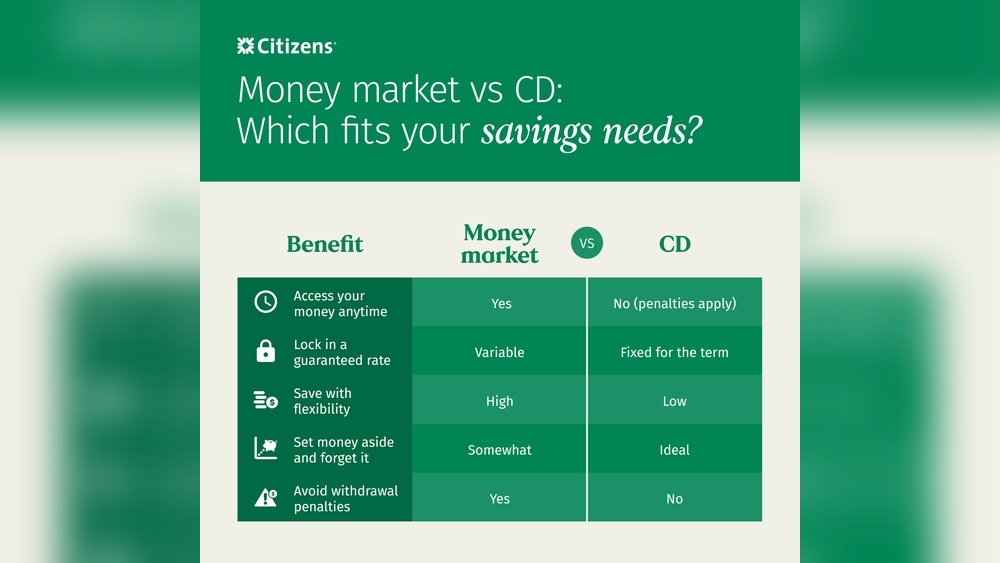

Money Market Account Vs Other Options

Savings accounts are simple and safe places to keep money. They usually offer lower interest rates but allow easy access to funds. Money market accounts often pay higher interest rates and allow limited check writing. They need a higher minimum balance than savings accounts.

Certificates of Deposit (CDs) lock money for a fixed time. They offer higher interest rates but you cannot withdraw money before the term ends without a penalty. CDs are best for those who do not need quick access to cash.

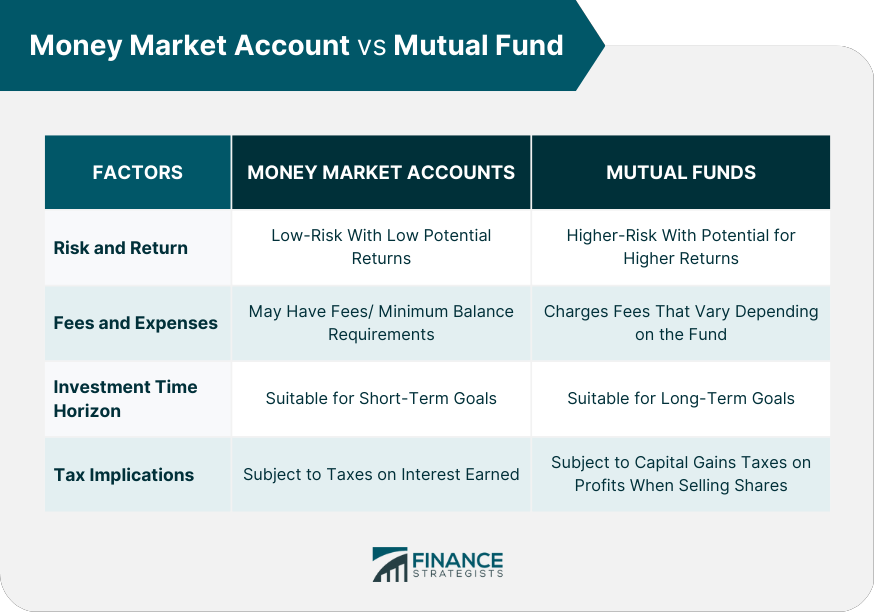

Money market mutual funds invest in short-term securities and are not insured by the FDIC. They tend to offer better returns than money market accounts but come with some risk. These are good for investors willing to accept small risks for better earnings.

How To Choose The Best Account

Evaluate your financial goals before choosing an account. Some accounts suit short-term savings, others fit long-term plans. Think about how often you need to access your money. Accounts with easy access help in emergencies. Others may limit withdrawals but offer higher interest. Compare fees carefully. Monthly fees can reduce your earnings. Some accounts waive fees if you keep a minimum balance. Look at benefits like check writing or ATM access. These add convenience but may come with costs. Use online comparison tools to see rates side by side. These tools also show fees and features clearly. They help find the best option for your needs quickly. Remember, the right account balances interest rates, fees, and access.

Top Money Market Accounts By Bank

U.S. Bank Elite Money Market offers a good APY with easy access to funds. It allows check writing but limits certain monthly transactions. Their minimum balance to avoid fees is moderate, making it suitable for many savers.

Citizens Bank Money Market requires a higher minimum balance to waive monthly fees. It provides a competitive interest rate and offers some check-writing privileges. Good for those who can maintain the required balance.

Merchants Bank Options features flexible account choices with varying minimum balances. Their rates are solid, and they have fewer transaction limits. Ideal for people wanting more control over their money market accounts.

| Bank | Minimum Balance | Monthly Fees | Check Writing | Transaction Limits |

|---|---|---|---|---|

| U.S. Bank Elite | Moderate | Waived with balance | Yes | Limited |

| Citizens Bank | High | Waived with balance | Yes | Standard |

| Merchants Bank | Varies | Varies | Yes | Fewer limits |

Credit Union Alternatives often provide better rates and lower fees. They may have more flexible terms and fewer restrictions. A great option for those wanting personalized service and local support.

Frequently Asked Questions

What’s The Best Money Market Account Right Now?

The best money market account currently offers competitive APYs around 4. 5% to 5%, with no monthly fees and easy access. Top choices include U. S. Bank Elite Money Market and Citizens Bank accounts. Always compare rates, fees, and transaction limits before deciding.

How Much Will $100,000 Make In A Money Market Account?

A $100,000 money market account can earn $200 to $600 annually, depending on the interest rate (0. 2%–0. 6% APY). Rates vary by bank and market conditions.

Where Can I Get 7% Interest On My Money?

You can earn 7% interest through high-yield investments like certain bonds, peer-to-peer lending, or riskier stock dividends. Traditional bank accounts rarely offer 7%. Consider money market funds or online platforms, but assess risks carefully before investing.

Who Has 4% Money Market?

Several banks and credit unions offer money market accounts with around 4% APY. Rates vary by institution and balance.

Conclusion

Choosing the right money market account depends on your needs. Compare interest rates, fees, and access rules carefully. Some accounts require higher minimum balances but offer better rates. Others provide easier access with lower fees. Remember, money market accounts are safe and FDIC insured.

They offer a good balance between savings and checking features. Review your options often to find the best fit. Your money works better when placed thoughtfully. Start with what suits your budget and goals. Keep checking for updates to rates and terms.

Read More

- Refinance Rate Lock Options: Secure Your Best Mortgage Deal Today

- Fixed Rate Mortgage Offers: Unlock Best Deals for Homebuyers Today

- Low Apr Loan Comparison: Find the Best Deals Today

- Private Banking Interest Offers: Unlock Exclusive High-Yield Benefits

- Home Equity Refinance Quotes: Unlock Savings with Top Rates Today

- Same Day Loan Prequalification: Fast, Easy Approval Tips

- Online Installment Loan Quotes: Unlock Fast, Easy Financing Today

- Prime Lending Rate Forecast: What Experts Predict for 2026

- Mortgage Refinance Approval Guide: Insider Tips for Fast Success

- Low Interest Personal Loans: Unlock Affordable Borrowing Today